The $5,000 Question

Let me paint you a picture. My cousin Sarah walked into a dealership last year with zero intention of leasing. She wanted to buy a new Honda CR-V. But the salesperson smiled, slid a piece of paper across the desk, and said: “Why pay $650 a month to own when you can drive this same car for $349 a month?”How Does Leasing a Car Work?

Sarah signed the lease that afternoon. A year later, she still doesn’t fully understand what a “money factor” is or why she has to worry about mileage. She just knows her payment is low and she gets a new car every three years.

But here’s the truth: leasing isn’t magic. It’s not better or worse than buying – it’s just different. And if you don’t understand how it works, you could end up paying thousands more than you need to.

In this guide, I’ll break down exactly how leasing a car works, using plain English and real numbers. No finance degree required.

What Is a Car Lease?

A car lease is essentially a long-term rental agreement. But instead of renting by the day (like Hertz or Enterprise), you’re renting for two to four years. You make a monthly lease payment to drive a brand-new vehicle, and at the end of the lease term, you return it to the dealership – unless you choose to buy it.

Here’s the key difference between leasing and buying:

| Leasing | Buying (Financing) | |

|---|---|---|

| Who owns the car? | The leasing company (lessor) | You (after final payment) |

| Monthly payment | Lower (you pay only for depreciation) | Higher (you pay for entire value) |

| End of term | Return, buy, or extend the lease | You keep the car (or sell it) |

| Mileage limits | Yes (typically 10k–15k miles/year) | No |

| Customization | Not allowed | Yes |

When you lease, you’re paying for the depreciation – the difference between the car’s selling price (capitalized cost) and its predicted value at the end of the lease (residual value). Plus interest (called the money factor) and fees.

Key Players in a Car Lease

Before we go further, let’s meet the characters:

- Lessee: That’s you. The person driving the car and making payments.

- Lessor: The leasing company. Often the manufacturer’s finance arm (e.g., Toyota Financial Services, Honda Financial Services, Ford Credit) or a bank like Chase Auto or Ally Financial.

- Dealership: The middleman. They sell the car to the lessor, who then leases it to you.

Understanding these roles helps you know who to negotiate with (the dealership on price, the lessor on terms).

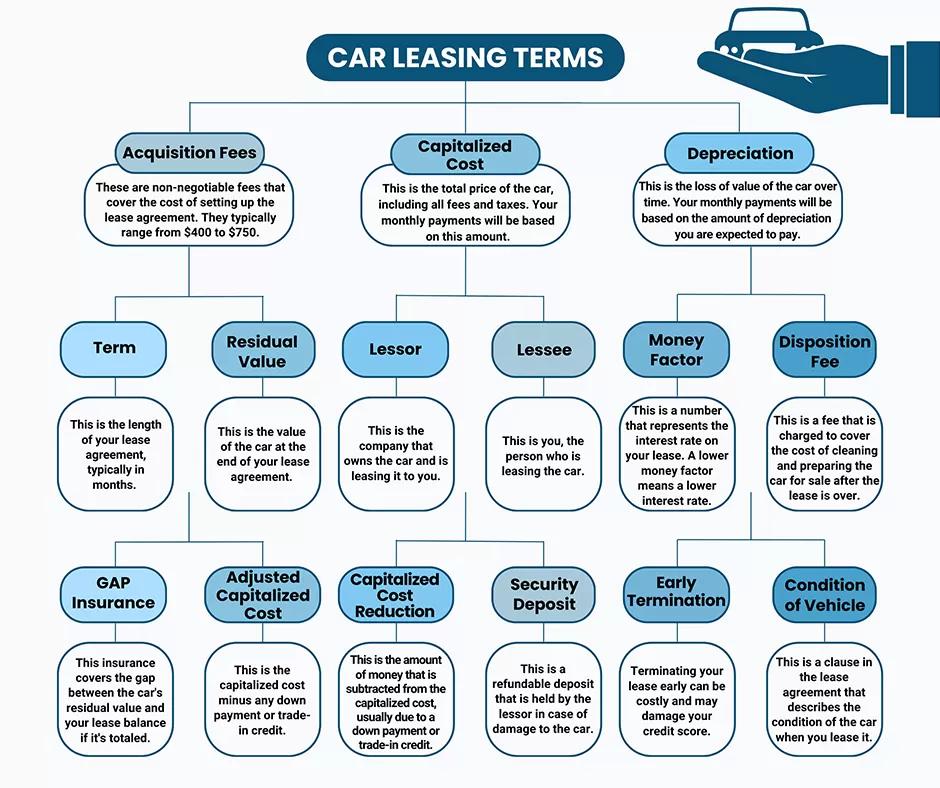

The 5 Core Components of a Car Lease

Every car lease agreement is built on five numbers. Master these, and you’ll never be confused again.

1. Capitalized Cost (Cap Cost) The Selling Price

This is the negotiated price of the vehicle – just like when you buy a car. Lower cap cost = lower monthly payment. Don’t skip negotiation just because you’re leasing. Dealerships expect you to haggle.

2. Residual Value The Future Worth

The leasing company predicts how much the car will be worth at the end of the lease term (usually 24–48 months). A higher residual value means you’re paying for less depreciation, so your monthly payment drops. Cars that hold their value well (Toyota, Honda, Subaru) often lease better.

3. Money Factor The Interest Rate

Instead of an APR, leases use a money factor a tiny decimal like 0.00125. Multiply it by 2,400 to get the approximate interest rate. For example:

0.00125 × 2,400 = 3% APR.

If a dealer won’t tell you the money factor, walk away

4. Mileage Allowance The Distance Limit

Most leases include 10,000, 12,000, or 15,000 miles per year. Exceed that, and you’ll pay an excess mileage fee – typically $0.15 to $0.25 per extra mile. Drive 5,000 miles over? That’s an extra $750–$1,250 at lease end.

5. Lease Term How Long You’ll Drive

Usually 24, 36, or 48 months. A 36-month lease is the most common. Shorter terms have higher payments (less time to spread depreciation). Longer terms risk paying for maintenance and tires.

How Monthly Lease Payments Are Calculated

Let me show you a real example. Suppose you lease a $35,000 car with:

- Negotiated cap cost: $33,000

- Residual value (after 36 months): $19,800 (60% of MSRP)

- Money factor: 0.00125 (3% APR equivalent)

- Miles/year: 12,000

Step 1: Depreciation Fee

($33,000 – $19,800) ÷ 36 months = $366.67/month

Step 2: Rent Charge (Interest)

($33,000 + $19,800) × 0.00125 = $66.00/month

Step 3: Total Base Monthly Payment

$366.67 + $66.00 = $432.67/month (plus taxes and fees)

That’s the math. Dealers may add acquisition fees, doc fees, or require a down payment (capitalized cost reduction) – which lowers the payment further but isn’t always smart (explained below).

Upfront Costs You’ll Pay When Leasing

Don’t be surprised by these fees at signing:

| Fee | Typical Cost | Purpose |

|---|---|---|

| Acquisition fee | $595–$995 | Processing the lease |

| Down payment (cap cost reduction) | $0–$2,000+ | Lowers monthly payment (optional) |

| First month’s payment | $300–$600 | Pay in advance |

| Security deposit | $0–$500 | Refundable (often waived) |

| Disposition fee | $300–$400 | Charged at lease end unless you buy the car |

Pro tip: Avoid putting money down on a lease. If the car is totaled, you lose that down payment. Roll everything into the monthly payment.

What Happens at the End of a Car Lease?

You have three main lease end options:

1. Return the Car and Walk Away

As long as you’re within the mileage allowance and there’s no excess wear and tear (dings larger than a credit card, torn seats, bald tires), you simply pay the disposition fee and hand over the keys.

2. Buy Out the Leased Car (Lease Buyout)

You can purchase the vehicle for the residual value plus any remaining fees. This is great if the car is worth more than the residual (you have equity). You can pay cash or get a car loan.

3. Trade In the Leased Car

Some dealerships allow you to trade in a leased car before the term ends, rolling any positive equity into a new lease or purchase. This is called a lease pull-ahead program.

4. Extend the Lease

If you’re not ready to decide, many lessors allow month-to-month extensions (usually up to six months).

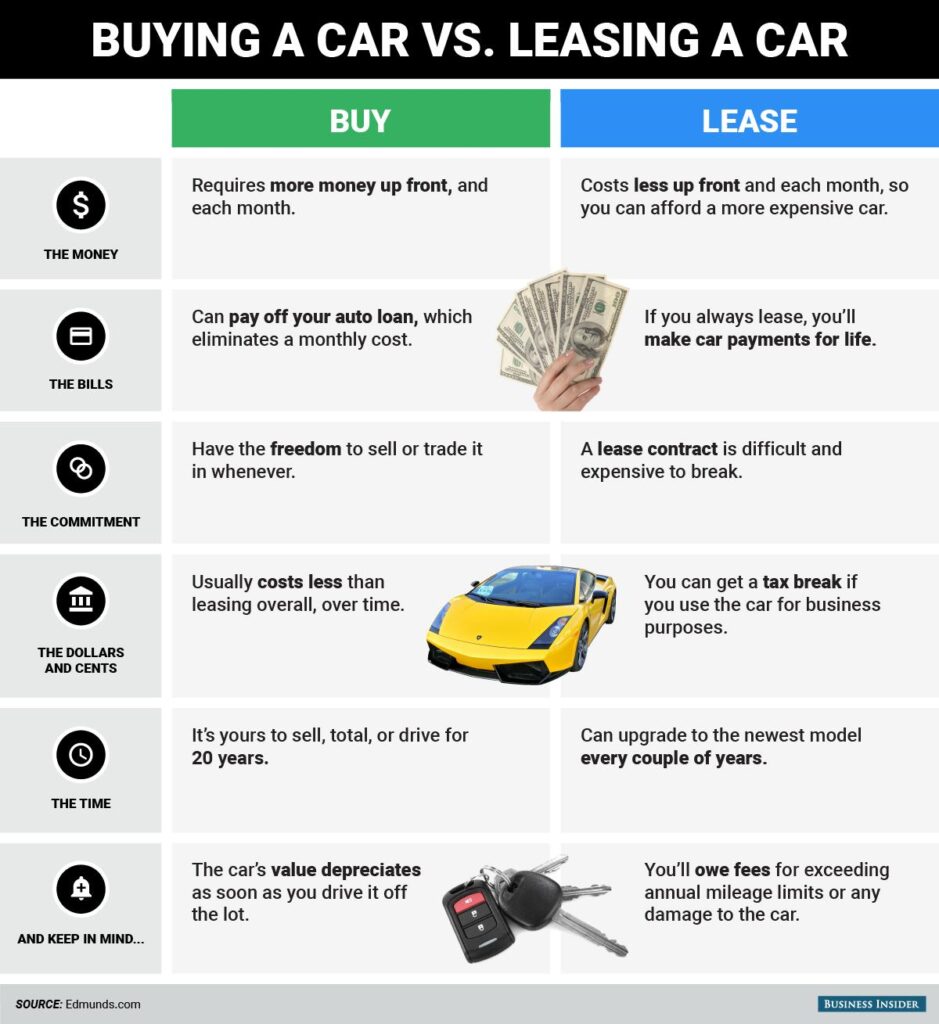

Leasing vs. Buying: Which Is Better?

This is the million-dollar question. Let’s be honest – neither is universally better. It depends on you.

You Should Consider Leasing If

- You like driving a new car every 2–3 years

- You want lower monthly payments

- You don’t drive more than 12,000–15,000 miles/year

- You prefer predictable maintenance (lease covers warranty period)

- You don’t want to deal with selling a used car

You Should Consider Buying (Financing or Cash) If

- You keep cars for 5+ years

- You drive a lot (over 15k miles/year)

- You want to customize or modify your car

- You hate having a car payment (eventually it ends)

- You want to build equity and have a trade-in asset

Real talk: Over the long term, buying is almost always cheaper. But leasing gives you lower payments and a new car every few years. It’s a lifestyle choice, not just a financial one.

Common Lease Mistakes And How to Avoid Them

I’ve seen smart people make these errors. Don’t be one of them.

Putting Money Down on a Lease

If you total the car driving out of the dealership, gap insurance covers the loan – but your down payment disappears. Roll it into the monthly payment instead.

Ignoring the Money Factor

Dealers love to hide this. Always ask: “What is the money factor, and what APR does that equal?” If they refuse, walk.

Not Negotiating the Cap Cost

People think lease prices are fixed. They’re not. Negotiate the selling price just like a purchase.

Forgetting About Gap Insurance

Most leases include gap insurance – it covers the difference between what you owe and the car’s value if it’s stolen or totaled. Confirm it’s in your contract.

Returning the Car With Excess Wear and Tear

A scratched bumper or cracked windshield can cost you hundreds at lease return. Get a pre-inspection before returning and fix minor issues yourself.

How Does Leasing a Car Work?

Q: Is leasing a car worth it for someone who drives 20,000 miles a year?

A: Probably not. Excess mileage fees ($0.15–$0.25/mile) add up fast. 5,000 extra miles per year = $750–$1,250 annually. You’re better off buying or looking into a high-mileage lease (rare).

Q: Can I negotiate a car lease like a purchase?

A: Absolutely. Negotiate the capitalized cost (selling price) first. Then discuss the money factor and residual value (those are set by the lessor but can sometimes be adjusted with loyalty programs).

Q: What credit score do I need to lease a car?

A: Most lessors want a score of 700+ for the best money factor. With a score of 620–699, you may still qualify but with higher interest (money factor). Below 620, leasing is difficult – consider financing a used car instead.

Q: Do I need gap insurance on a lease?

A: Yes, and most leases include it automatically. Gap insurance protects you if the car is totaled and you owe more than its actual cash value. Always confirm it’s in your contract before signing.

Q: Can I return a leased car early without penalty?

A: Early termination fees can be brutal – often the sum of all remaining payments plus the disposition fee. Some manufacturers offer lease pull-ahead programs if you lease another car from them. Otherwise, you might be better off paying to the end or finding someone to transfer the lease.

Leasing Isn’t Scary If You Understand It

When my cousin Sarah asked me recently, “Did I make a mistake leasing?” – I told her no. She loves having a new car, she drives under 12,000 miles a year, and she hates selling cars. For her, leasing works.

But for her brother Dave, who commutes 25,000 miles a year and keeps his cars for a decade? Leasing would be a disaster.

How does leasing a car work? It works by trading long-term ownership for lower monthly payments and the joy of driving new vehicles. It’s not a scam, and it’s not a ripoff. It’s a tool. Use it when it fits your life.

Now I want to hear from you. Have you leased a car before? Would you consider it after reading this? Drop a comment below – I read every single one.

And if this guide helped you, share it with a friend who’s about to walk into a dealership. You might just save them thousands.